As we move through late 2025 and into 2026–2027, small businesses face a mix of opportunity and risk. The macroeconomic backdrop suggests modest growth, lingering inflationary pressures, and shifting consumer behavior. Understanding the data and likely scenarios can help small businesses plan better — for hiring, pricing, investment, and cash flow.

Current Context: Strengths & Weaknesses

To assess what’s ahead, let’s first review where things stand.

Key Indicators & Trends

GDP & Growth

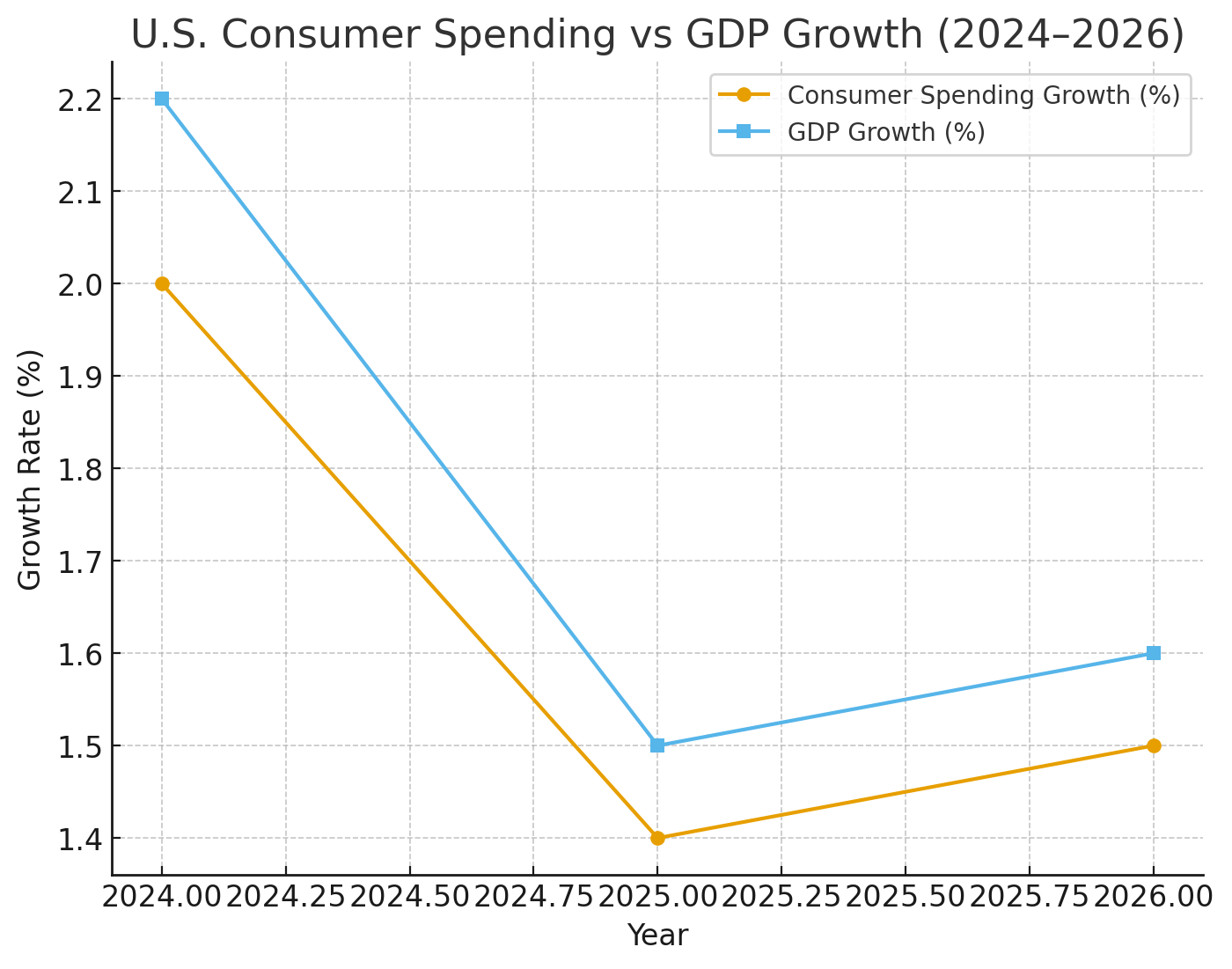

Real GDP shrank in Q1 2025 by 0.5% (annualized), marking the first contraction in several years. AmPac Business Capital

Forecasts for the rest of 2025 expect a modest rebound: growth rates of ~1.4%–1.5% for GDP in 2025–2026. EY+2Deloitte+2

Consumer Spending

Spending growth has slowed sharply: in early 2025, consumer spending grew only ~0.5%, its weakest pace since 2020. AmPac Business Capital

Forecasts: real consumer spending up ~1.4% this year, and about 1.5% in 2026. Deloitte+1

Breakdown: durable goods and big-ticket items (houses, cars, appliances) are more sensitive to high interest rates and tariffs; nondurable goods and services are relatively more stable. Deloitte+1

Inflation & Interest Rates

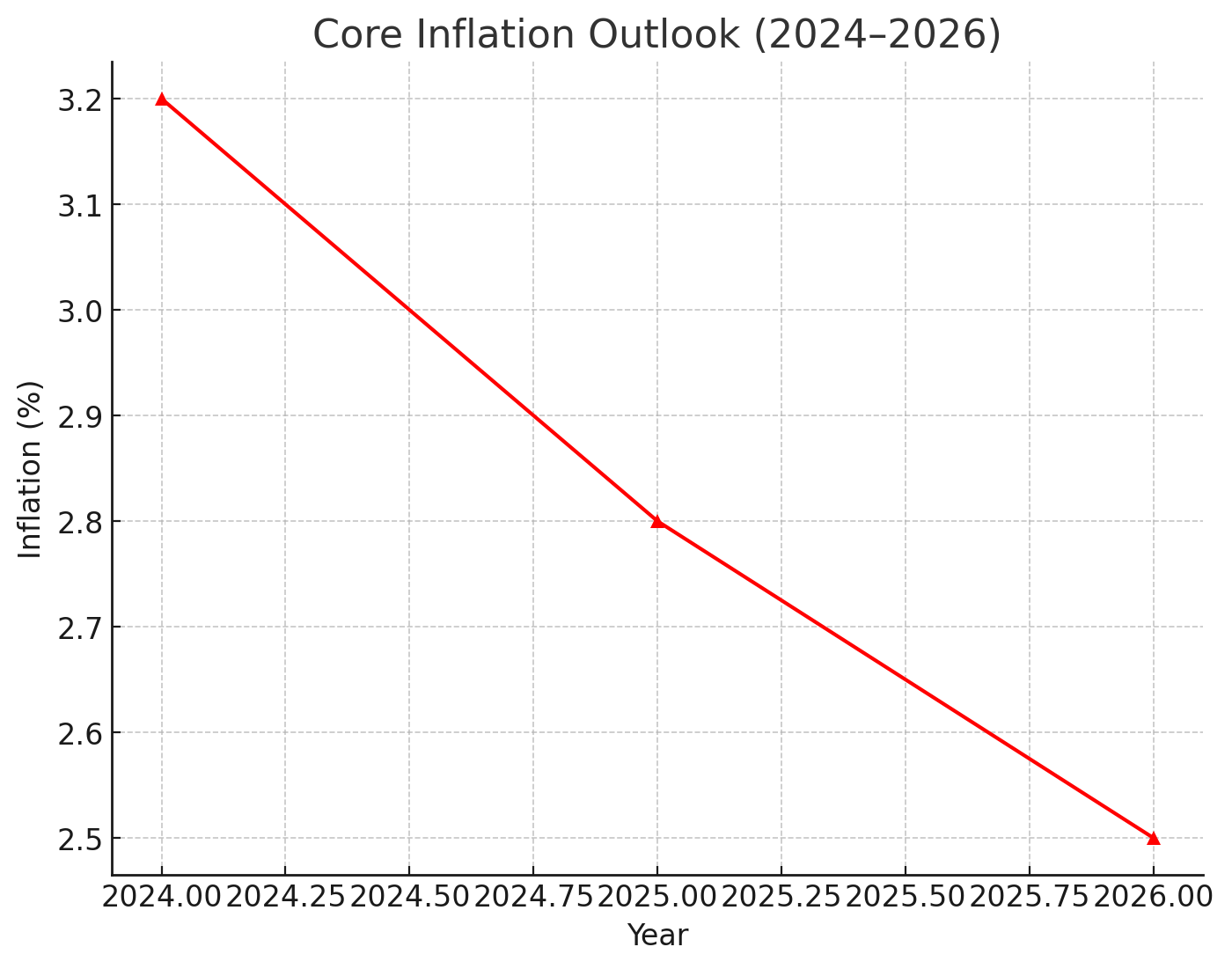

Inflation remains above many policy targets (e.g., Federal Reserve has a long-run target around 2%). Some measures (core inflation, services inflation) continue to be sticky. AmPac Business Capital+1

Interest rates have been elevated to counter inflation. The cost of borrowing (for consumers and businesses) remains a headwind, especially for small businesses with less margin or heavy debt load.

Labor Market & Consumer Sentiment

Unemployment is relatively low (in the ~4–4.5% range) though signs of cooling are appearing in hiring and job-opening trends. AmPac Business Capital+1

Consumer confidence is mixed. Some optimism exists, but many households are expressing concerns about rising prices, incomes, and future economic uncertainty. McKinsey & Company+2Federal Reserve Bank of New York+2

Business Sentiment / Small Businesses

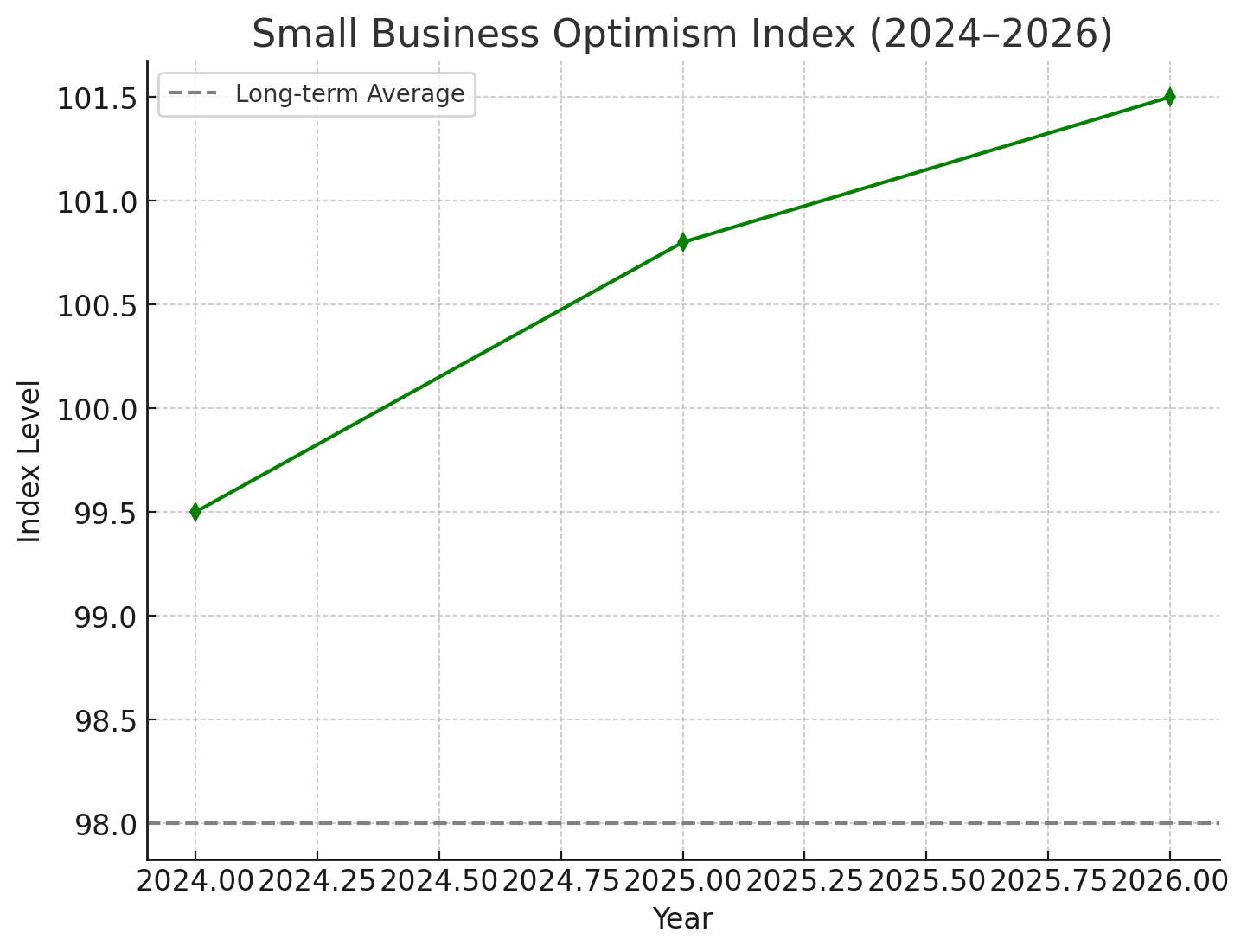

The NFIB (National Federation of Independent Business) Small Business Optimism Index ticked up slightly in August 2025 to ~100.8, just above its long-term average of ~98. NFIB - NFIB Small Business Association

But survey data suggest growing cautiousness: many small business owners are less likely to expand, hire, or invest aggressively due to policy uncertainty (tariffs, regulation), rising costs, and concerns about consumer demand. AmPac Business Capital+2NFIB - NFIB Small Business Association+2

What This Means for Small Businesses & Consumer Behavior

With the above in mind, here are some likely trajectories and how they’ll impact small players and consumers.

Scenario | What it looks like for small business | What it looks like for consumers |

|---|---|---|

Modest Growth / Soft Landing (favored by many forecasters) | Small businesses may see slow but steady sales growth; pricing power remains limited; margins squeezed by input and borrowing costs; cautious hiring; focus on cost control and incremental investment. | Consumers prioritize essentials; discretionary spending (travel, luxury, big-ticket items) will grow slowly; many households will reduce discretionary budgets; some will dip into savings or use credit for large purchases. |

Slowdown / Mild Recession | More serious risk if inflation persists or a policy misstep occurs; small businesses may see falling demand, tighter credit, pressure from rising costs; some layoffs or scaling back; survival depends on adaptability. | Consumers become more risk-averse; postponement of large purchases; increased price sensitivity; more discount and deal hunting; shift toward cheaper alternatives; possibly increased debt or reduced saving. |

Upside Surprise – inflation cools faster, tight labor markets ease, policy clarity improves | If conditions improve, small businesses that invested smartly could benefit from pent-up demand, especially in sectors like services, home improvement, local retail; some rebound in expansion and staffing. | Consumers gain more discretionary income; confidence returns; rebound in non-essentials; more spending on experience, travel, entertainment. |

Expected Trends Over the Next 2-3 Years (2026–2027)

Here are some more specific forecasts/trends to watch, especially for small business owners:

Spending Composition Will Shift

Services and nondurables likely to outperform durables. Products with long replacement cycles (cars, appliances) will underperform unless interest rates come down or credit becomes more accessible. Also, online and discount channels may gain further ground.Pricing & Margin Pressure

Rising costs (labor, energy, raw materials), tariffs, and supply chain disruptions will continue to squeeze margins. Businesses with good operational efficiency, flexible supply chains, or ability to pass on price increases will fare better.Borrowing Costs & Access to Capital

Elevated interest rates mean loans, lines of credit, and refinancing will be more expensive. Small businesses with weaker credit profiles may struggle. Those with stronger cash reserves or alternative financing will have an advantage.Labor & Talent Constraints

Even as unemployment edges up, labor quality, retention and cost will remain concerns. Some businesses will still struggle to recruit/wage competitively, especially in skilled or semi-skilled sectors.Consumer Behavior & Expectations

Consumers are likely to become more price-sensitive; promotions, value offerings, loyalty programs will be more powerful. There's also likely to be increased interest in flexible payment options (“buy now pay later”), second-hand options, and delaying non-urgent purchases.Regulatory & Policy Uncertainty

Tariffs, trade policies, fiscal spending, regulation of AI/technology, healthcare, etc., may change; shifts could impose sudden costs or open opportunities.Regional & Sectoral Variation

Outcomes will not be uniform. Small businesses in regions with higher cost of living, tighter labor markets, or exposure to trade may face more headwinds. Some sectors (hospitality, travel, food services) may rebound more strongly; others with discretionary luxury goods may lag.

Data & Projections at a Glance

Real consumer spending growth: ~1.4% in 2025; ~1.5% in 2026. Deloitte+1

GDP growth: ~1.5% in 2025; similar modest growth in 2026. EY+1

Inflation (core / services): likely to remain above target (2%) for at least the next year, gradually cooling if supply chains and policy stabilize. AmPac Business Capital+1

Consumer income expectations: median expected income growth ~2.9% in the near term. Federal Reserve Bank of New York

Consumer spending expectations (households): growth expectations around 5.0% in some surveys for next 12 months. Federal Reserve Bank of New York

Small business optimism: NFIB’s index ~100.8 in August 2025 (slightly above long-run average). NFIB - NFIB Small Business Association

Strategic Implications & Advice for Small Businesses

Based on this outlook, small businesses can take proactive steps to be resilient and take advantage of opportunities.

Focus on flexibility and cost management

Build buffers (cash flow, inventories) to absorb shocks from rising costs or supply chain delays.

Explore cost efficiencies: renegotiate supplier contracts, reduce waste, adopt more efficient technologies.

Monitor customer behavior and adjust offerings

Track which product lines are slowing (durables, luxury) vs. which are picking up (essentials, value, services).

Consider bundling, loyalty incentives, or value versions of products to retain customer base.

Pricing strategy

Be transparent when increasing prices (due to costs), as consumers are sensitive.

Use dynamic pricing or tiered pricing where possible to balance margins and volume.

Invest selectively

Prioritize investments that improve customer satisfaction or retention (digital tools, customer service, streamlined operations).

Be cautious about large capital expenditures unless there is a clear ROI and manageable financing.

Manage debt and financing prudently

Lock in favorable terms if possible; avoid over-leveraging.

Explore alternative financing if traditional lending is tight or expensive.

Scenario planning

Develop best case / base case / downside case plans (e.g. what do you do if demand falls 10% or inflation rises another point?).

Stress-test your business for different interest rate, supply cost, and consumer demand outcomes.

Risks & Wildcards

A few things could significantly alter the picture, either for better or worse:

A sharper than expected decline in inflation, allowing central banks to reduce rates more quickly.

Sudden tightening of labor markets or supply chain disruptions (e.g. geopolitical risk, climate events) that drive costs.

Policy shifts: new tariffs or trade policies; tax changes; regulation of sectors like tech/AI.

Changes in consumer credit – e.g., widespread defaults or tightening of credit availability could rapidly reduce consumer spending.

Shocks (pandemic-like or geopolitical) that affect global supply chains, energy, or consumer behavior.

Conclusion

Small businesses are operating in a period of modest growth, uneven headwinds, and cautious optimism. Consumer spending is holding up, but the pace is slowing, and cost pressures are real. Businesses that act with agility, keep a close eye on their cost structure and cash flow, understand changing consumer expectations, and prepare for several possible scenarios will be better positioned.

Consumer Spending vs. GDP Growth (2024–2026) – trending down to modest levels.

Core Inflation Outlook (2024–2026) – inflation cooling but still above the Fed’s 2% target in the near term.

Small Business Optimism Index (2024–2026) – sentiment rising slightly above the long-term average, but still cautious.

Are you looking to promote your business and are overwhelmed with where to start? Here are 5 ways to promote your business.

1. Leverage Social Media Marketing

Platforms like Instagram, Facebook, TikTok, and LinkedIn can help build your brand, show off your work, and engage with your audience. So many business owners become overwhelmed with running the business that their social media gets put on the back burner. It’s a free and easy way to get your business out there to hundreds, thousands, sometimes millions of viewers.

Share behind-the-scenes content, customer testimonials, before-and-after shots (especially great for service businesses like cleaning or food).

If you are too busy to keep up with running your social media, I suggest hiring someone. Hiring someone local is best because they can take photos, videos and get a real sense of the business. But if you need cheaper options, Upwork and Fiver are good alternative options.

2. Use Google My Business (GMB)

Claim and optimize your Google Business Profile so people can find you in local searches.

This is a common mistake I see a lot of business owners make. They create their website, set up their social media and forget about creating their Google Business profile.

81% of consumers use Google to evaluate local businesses, and a 63% are likely to check Google reviews before visiting a business.

As a business owner you want to get reviews, add photos, update hours, and post updates. Also do not wait for customers and clients to review, ask for them, send emails and texts letting them know their review really helps a business grow. A great way is to create some reward like a discount for leaving a review.

3. Referral Incentives & Word of Mouth

Encourage happy customers to refer others by offering discounts or perks.

Word of mouth is still one of the most powerful tools—people trust people.

One of the best referral programs is to offer a discount to your frequent customer and to the one they are bringing in. For example if customer A brings in their friend,customer B, both people get a discount. While you might lose a little profit on that exact sale, you have not only made customer A happy and proud to bring in their friend to a new business, you now have a high potential of gaining customer B as a repeat customer.

4. Local Partnerships & Events

Team up with local businesses, sponsor community events, or attend farmers markets, festivals, and pop-ups.

Networking and being visible in the community can help a business build local support.

Donate your time to other organizations and businesses, donate money if you have it and be advocates for other businesses so they can be advocates for you.

I can’t tell you how networking and being involved in the community has helped me grow personally and professionally.

5. Online Ads (Targeted & Local)

Invest in Google Ads, Facebook/Instagram ads, and even platforms like Nextdoor to target specific areas and demographics.

Online ads are not for everyone and take work. If you do not know what you are doing in this area please consult with someone in marketing, watch youtube video or read up on this topic on the internet. While businesses can have great success with it, if you don’t know what you are doing, you can waste a lot of money and time as well.

Start small, test, and refine what works.

And those are my top 5 reliable ways to promote your business. Would love to hear what has worked for you in the comments so we can help each other learn as well.